How Do Retail Stores Compete in an FMCG Market?

Lessons From the Acquisition by Shoprite of Select Massmart Stores

-

June 01, 2023

Downloads Download Article

Download Article

-

This article discusses market definition and the assessment of competition in retail mergers, and specifically in fast moving consumer goods (“FMCG”) markets. It considers recent analysis conducted by FTI Consulting for a large retail grocery chain in South Africa.

During 2021, Shoprite announced that it was acquiring certain Massmart stores, branded either Cambridge or Rhino. The transaction included (i) wholesale and retail grocery; (ii) and liquor stores; (iii) a meat processing facility (Massfresh Meats); and (iv) a wholesaler and distributor of fresh fruit and vegetables (Fruitspot). The merger was conditionally approved by the South African Competition Tribunal on 9 December 2022. At the time of writing, the reasons for the decision have not yet been published.1

This article focuses on market definition and the assessment of competition around 56 Cambridge and Rhino stores acquired by Shoprite. Massmartʼs prior sale of various Cambridge and Rhino stores to Devland in early 2021 resulted in valuable South African case precedent on market definition. However, the larger scope of this transaction required that FTI Consulting conduct a more technical analysis. We therefore constructed a dataset of all potential stores within the local catchment areas and relied on Geographic Information Systems (“GIS”) tools to analyse the boundaries of these local markets. More sophisticated techniques provide the analyst a more formal approach to consider all potential competitors within the relevant area. We expand on this approach in this article.

The Challenge – Product and Geographic Market Definition in FMCG Markets

Various factors determine the product and geographic dimensions of market definition in retail mergers. Amongst others, these include the basket of goods sold, whether there are sub-markets by grocery segment (e.g., chilled vs dry goods), whether all customers fall into one larger market, whether they should be segmented by income category, or how far a consumer is willing to travel to reach retail outlets.

South African case precedent generally defines grocery retail product markets as retail grocery markets (including all products sold by a grocery retail chain, excluding liquor). The current case focused specifically on two elements. The first of these was whether separate markets exist that cater for low-income consumers. Secondly, it focused on whether independent stores offer a competitive constraint to the merging parties and should therefore be included in the relevant product market.

Generally, in retail mergers, geographic markets are defined as either national or local. This is because supermarket chains operate at a national (or at times regional) level, while consumers shop in a local area.

The South African competition authorities have generally followed international precedent in this regard and have defined markets in a similar manner in the many retail mergers that they have analysed.

This merger placed significant focus on local market dynamics. While national market shares were relevant, the competition authorities were interested specifically in local markets, and in how the transaction affected consumer choice in these markets. As a result, FTI Consultingʼs task was to analyse competition dynamics within 56 distinct local areas across the country. GIS analysis was instrumental in managing this data intensive exercise.

Using GIS to Define the Geographic Boundaries of Local Markets

Merger assessments in South Africa have generally used a fixed radius (between 1.5km and 3km) from the target stores to consider boundaries of the local markets in retail grocery cases.2 In this case, FTI Consulting employed a more sophisticated tool in the form of an isochrone analysis. While a fixed radius does not provide any information such as travel patterns and traffic, for example, an isochrone analysis can determine the areas that can be reached from a particular location within a given time, taking account of various features of the catchment area. Isochrone analysis is prevalent in retail grocery mergers in many international jurisdictions, including the UK3 and the European Union.4

An analysis of isochrones can take account of factors beyond those considered in a conventional competitive effects analysis. Examples of these factors include:

- The distance between the point of origin and all other points within the catchment area;

- The travel time between the point of origin and all other points within the catchment area (which can be impacted by mode of transportation, road conditions, and speed limits);

- The mode of transportation (such as walking, cycling, driving or public transportation); and

- Whether the catchment area is urban, rural, or a combination of both.

One of the primary benefits of using an isochrone analysis over a simple “as the crow flies” radius approach, is that isochrones consider real-world factors

While a radius approach simply assumes one can travel the same distance around a point in the same amount of time, regardless of factors such as road conditions, speed limits, and proximity to a highway, an isochrone approach accounts for these factors.

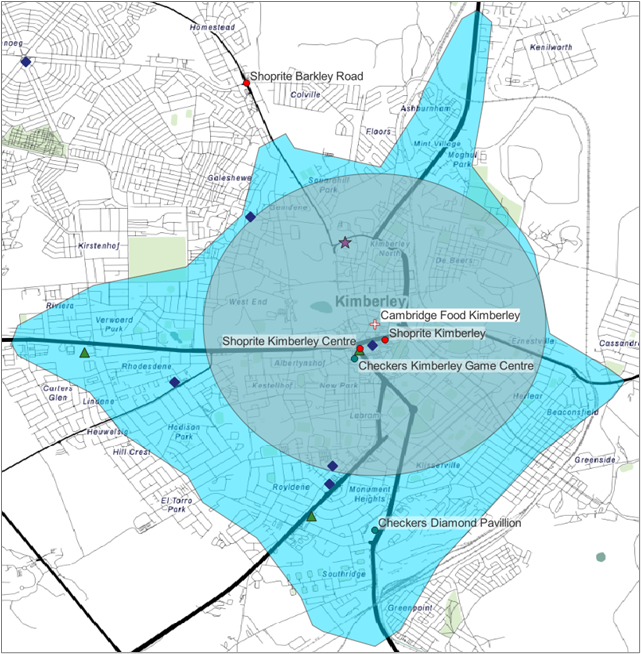

Figure 1 below provides an illustrative example of this concept. It shows the catchment area for a simple 2km radius (inner grey circle), and a five-minute drive- time isochrone (outer light blue polygon) around the Cambridge store in Kimberley, a medium sized mining town in South Africaʼs Northern Cape province. A radius approach provides a catchment area that is somewhat arbitrary. However, a five-minute drive-time isochrone, takes account of the geographic conditions around the Cambridge store when determining the catchment area. For instance, in five-minutes, one can travel farther to the West of the store than to the East. This is because the road to the West is a national road (the N8), while the road leading to the East is a regional road (the R64).

Figure 1: Example of 2km Radius (Inner Grey Circle) and 5-Min Drive-Time Isochrone (Outer Light Blue Polygon) Around Cambridge Food Kimberley Location

Source: Map © Thunderforest; Data from FTI Consulting analysis and obtained from merger parties

Using spatial analysis, FTI Consulting was able to map all relevant stores within various radii and isochrones, allowing for a more complete view of competition within a given local area. While the coordinates for Shoprite and Cambridge stores were readily available from the merging parties, FTI Consulting constructed a comprehensive database of other major retailers (such as Spar, Pick ʻn Pay, etc.) from publicly available information. FTI Consulting collected data on store locations on the My Catalogue website, which publishes up-to-date catalogues and specials from leading retailers. My Catalogue operates primarily as a platform for the sharing of catalogues but includes detailed information on store locations5 for a range of retailers (in the form of physical addresses). FTI Consulting constructed a database of these addresses, and relying on GIS software, geocoded6 these addresses to obtain their spatial coordinates (latitude and longitude). In addition, FTI Consulting could ascertain the locations (and spatial coordinates) of various independent retailers. Through engagements with the merging parties, FTI Consulting identified the independent retailers exerting a competitive constraint on the merger partiesʼ stores in the relevant catchment areas.

Figure 1 also shows the Cambridge store, the Shoprite owned stores (Shoprite as red dots and Checkers as green dots in this example), as well as the identified Pick ʻn Pay stores (blue diamonds), Spar stores (dark green triangles), and an independent store (purple star) that fall within the relevant catchment area in Kimberley. Using a simple radius captures only those stores in close proximity to the Cambridge store. However, an isochrone provides a more complete picture of competition, including stores that are more easily accessible via the road networks. Having established the appropriate methods to construct the boundaries of the local markets, FTI Consulting analysed competition in these markets. Relevant questions arising were: (i) which competitors should be included in the analysis; and (ii) how best to assess competition between these competitors in the local markets (both pre and post-merger).

Assessing Competition In Local Retail Grocery Markets

Who Should Be Included in the Competitor Set?

FTI Consulting found that the product market included all products sold by a grocery retail chain. However, when assessing competition and the impact of the merger in each local market, an important analytical question arose: Should the local market be limited to large national retailers, or should it include challenger retailers, independent retailers or even spaza shops? Indeed, many independent stores offer the same range and/or depth of products as national retailers and therefore compete in the same product market.

To construct the competitor set, FTI Consulting developed specific criteria to assess the competitive constraint offered by various independent stores to the merging parties in the local markets. Specifically, FTI Consulting considered an independent store to be a competitive constraint where it offered sufficient breadth and depth of products. Broadly speaking, these relate to:

- Whether the store stocked a similar range of products as Shopriteʼs top selling products; and

- Whether the number of SKUs was sufficiently high to be considered an alternative to larger retailers.

Several other criteria were investigated, such as whether an independent store was part of a buyer group, the size of the storeʼs gross letting area, its proximity to transport nodes, and so on. This was largely informed through interactions with the Competition Commission and by obtaining ground-level information from the merging parties. The analysis excluded independent stores who did not meet the criteria.

FTI Consulting highlighted the degree of competitive constraint offered by spaza shops, due mainly to their proximity to consumers and the similarity of their basic product offering. The South African Competition Commissionʼs Grocery Retail Market Inquiry (“GRMI”) identified spaza shops as offering a degree of competitive constraint to larger retailers. In particular, the constraint exists when consumers do “top-up” shopping on a more frequent basis.7, 8 Ultimately, FTI Consulting excluded these stores from the final structural analysis but noted that they collectively exert a degree of competitive constraint on larger retailers.

How To Measure Competition and the Effect of the Merger at the Local Level?

Having defined 56 local markets and their competitor sets, the merger assessment turns to competitive effects. This required an analysis of the state of competition within each market prior to the merger, and of how the merger would affect competition in each market. This presented many challenges. Detailed information for each store in the 56 areas was not readily available to calculate metrics such as revenue market shares, which typically inform competition analyses. Therefore, FTI Consulting calculated metrics which offer insights into consumer choice, such store count and fascia count.

Following international precedent from the Competition and Markets Authority (“CMA”) in the UK, FTI Consulting adopted a fascia approach as an initial screening tool for a structural analysis. The fascia count aggregates all stores within a group-ownership structure (i.e. fascia) and counts them as one. The fascia count captures the importance that consumers attach to a brand. Fascia counts may be useful in specific cases where the analyst is interested in consumer choice. The FTI Consulting analysis combined both store count and fascia count to get a picture across all dimensions of competition. Store count is another standard metric available to consider the structural effect of a merger. This is useful when revenue at a local level is not available for all candidate stores.

The CMA has previously suggested that a merger giving rise to a four-to-three fascia count within a geographic market may raise concentration concerns (all else equal).9 In this case, FTI Consulting used fascia and store counts to provide a comprehensive view of the structural effects of the merger, and to account for different features and shortcomings of both metrics. However, different jurisdictions have applied fascia and store counts in different ways, depending on the specifics of the case.

Further GIS Applications in Competition Assessments

With increasing data availability and developments in technology, GIS analysis has become a powerful tool in competition analysis. Competition authorities accept its use, and its more frequent use allows for large- scale, nuanced, and robust analyses. This is a positive development in merger analysis. FTI Consulting has also used GIS to analyse the dispersion of customer revenue and disposable income in different geographical areas, and to map telecommunication networks throughout South Africa to understand the overlap between networks. These tools are likely to become widely used in competition analysis going forward.

To Illustrate the Differences Between Fascia and Store Count, Consider the Following Hypothetical Example:

- Suppose a geographic market contains the following stores: Four Shoprite stores, two Checkers stores, one Cambridge store, two Spar stores, three Pick ʻn Pay stores, two Boxer stores, and one Hypercheck store.

- The pre-merger store count would be 15.

- Shoprite and Checkers (with common ownership) would have a 40 percent market share, and Cambridge would have a 7 percent market share.

- On a store count basis, the merger presents an accretion in market share from 40 percent to 47 percent. Evaluated in isolation, this raises a potential competition concern.

- In contrast, the fascia count would be five, since Shoprite and Checkers (with common ownership) count as one fascia, and Pick ʻn Pay and Boxer (with common ownership) count as one fascia.

- Post-merger, the fascia count reduces to four, as Cambridge now forms part of the Shoprite fascia.

- According to CMA precedent, a reduction to four fascias does not present a structural concern, as there would still be sufficient consumer choice in the area.

- A combination of these methods is therefore usually preferable to relying on only one metric.

*FTI Consultingʼs Professor Nicola Theron acted as the expert witness for the merging parties and was assisted by Wimpie van Lill, Albertus van Niekerk and Dr Roan

Footnotes:

1: On 9 December 2022, the Competition Tribunal conditionally approved the large merger whereby Shoprite Supermarkets (Pty) Ltd (“Shoprite”) acquired certain wholesale and retail supermarket and liquor stores, as well as the Massfresh business from Massmart Holdings Limited (“Massmart”). FTI Consulting (“FTI”)*, instructed by DLA Piper Advisory Services, acted as economic experts for the merging parties and provided economic analyses throughout the merger assessment process. The economic analyses conducted by FTI Consulting encompassed data gathering, complex data analysis, writing expert economic reports and providing expert witness testimony at the Competition Tribunal hearing. FTI Consulting also assisted in developing the final conditions that led to the approval of the merger.

2: For instance, in Mystic Blue/Rhino (case no. 35/LM/Apr11), the Commission identified a 1.5km radius surrounding the main taxi ranks in the towns where the partiesʼ activities overlapped. Similarly, in the SPAR Groupʼs acquisition of the Florida Junction and Gordon Road SUPERSPAR stores (case no. 020925) and in SPAR/Western Gruppe Trading (case no. LM040May19), it identified a 1.5km radius around the target stores. In Shoprite/Gaterite Hypermarket (case no. 018226) and in the recent Devland/ Masscash merger (case no. LM163Dec20), it identified a 2km radius around the target firm. In Shoprite/Foodworld (case no. 47/LM/Jun05) and Pick ʻn Pay/Trio Bellville (case no. LM252Mar15), the Commission identified the catchment area as being within a 3km radius around each target store.

3: See for instance CMA Report in the Tesco/Booker transaction.

4: See for instance European Commission DG Competition Report in the Salling Group/Tesco Polska merger.

5: Examples of store chains on the My Catalogue website include, amongst others, Boxer, Choppies, Food Lovers Market, Pick ʻn Pay, SPAR and various other independent store chains (such as Devland Cash & Carry, Jumbo Cash & Carry, etc.).

6: Geocoding is the process of converting a textual address/location description into geographic coordinates that can be inputted into GIS software.

7: The GRMI report states that, “The results of the survey suggested that consumers across income bands make use of more than one outlet for their shopping needs. Some consumers consider supermarkets to be interchangeable with spaza shops and wholesalers. Based on the survey, customer behaviour differs when shopping for convenience i.e., daily shopping as opposed to weekly shopping.” Competition Commission. (25 November 2019). Grocery Retail Market Inquiry Final Report, p.68, para 99.

8: The consumer survey from the GRMI also shows that, “spaza shops are used almost exclusively for daily/ convenience shopping. However, the data also reveal that consumers make use of local supermarkets for their daily or convenience shopping. Interestingly, the survey shows that the top five products in the monthly grocery bag and the convenience bag are similar. These are maize meal, rice, meat (beef or pork), bread and cleaning products.” Competition Commission. (25 November 2019). Grocery Retail Market Inquiry Final Report, p. 120-121, para 279.

9: Competition & Market Authority. (2017). Retail mergers commentary. Page 23.

Published

June 01, 2023